Capital gains tax

Contents |

[edit] Overview

Capital Gains Tax (CGT) is levied on the profit that is made when something is sold, gifted, swapped or otherwise disposed of.

The following assets are liable to Capital Gains Tax:

- Property. If it is not the main home (unless it is let out, used for business or larger than 5,000 square metres).

- Shares that are not in a NISA, ISA or PEP.

- Personal possessions that are worth more than £6,000 (apart from a personal car).

- Business assets.

- Overseas assets.

[edit] Property

Property that is liable to Capital Gains Tax includes:

- Second homes.

- Any rental properties.

- Business premises.

- Land, including agricultural land.

The selling of a main home will not generally be liable to Capital Gains Tax and may be eligible for Private Residence Relief.

[edit]

The investments that are liable to Capital Gains Tax include:

[edit] Personal possessions

The majority of personal possessions that are worth more than £6,000 are liable to Capital Gains Tax, including:

- Jewellery.

- Antiques.

- Paintings.

- Coins and stamps.

- Possessions that are part of a set, such as matching vases (the threshold applies to the set as a whole).

[edit] Business assets

Numerous business assets are liable to Capital Gains Tax and typically include:

- Buildings and land.

- Fixtures and fittings.

- Shares.

- Plant and machinery.

- Goodwill.

- Registered trademarks.

[edit] Overseas assets

For residents in the UK, overseas assets are liable to Capital Gains Tax, including:

- Holiday homes.

- Shares in a foreign company.

- Land abroad purchased for development.

[edit] When Capital Gains Tax is not required

Capital Gains Tax is only required on any gains which are in excess of the tax-free allowance, which for 2013-2014 is:

- £10,900 for individuals.

- £5,450 for trustees.

It is not normally necessary to pay Capital Gains Tax on gifts between husband and wife, civil partner or to charities. In addition, Capital Gains Tax on inheritance is typically only required when an asset is sold.

The following assets are not liable:

- Personal car.

- Personal possessions that are disposed of for less than £6,000.

- Main home.

- Any tax free investment savings accounts e.g. ISAs and PEPs.

- Winnings from the lottery, betting or the pools.

- UK government gilts and Premium Bonds.

- Personal injury compensation.

- Foreign currency for personal use.

[edit] Rates for Capital Gains Tax

The rates for Capital Gains Tax for 2013-14 are:

- 18% and 28% for individuals (dependent on the total amount of taxable income).

- 28% for trustees or for personal representatives of someone who has died.

- 10% for sole traders or partnerships with gains qualifying for Business Asset Disposal Relief or BADR (formerly known as Entrepreneurs' Relief).

[edit] Reporting Capital Gains Tax

If Capital Gains Tax needs to be paid, HM Revenues and Customs (HMRC) will require notification through a tax return. This can be completed online or alternatively on paper.

[edit] Record keeping

It is necessary to maintain any records for at least one year after the Self Assessment deadline and businesses must maintain records for 5 years after the deadline.

[edit] Related articles on Designing Buildings Wiki.

- Business Asset Disposal Relief BADR.

- Business rates.

- Capital.

- Capital allowances.

- Capital gain.

- PAYE.

- Stamp duty.

- Taxes associated with selling a business.

- Tax relief.

- VAT.

[edit] External references

Featured articles and news

Farnborough College Unveils its Half-house for Sustainable Construction Training.

Spring Statement 2025 with reactions from industry

Confirming previously announced funding, and welfare changes amid adjusted growth forecast.

Scottish Government responds to Grenfell report

As fund for unsafe cladding assessments is launched.

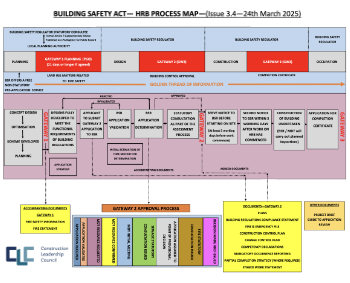

CLC and BSR process map for HRB approvals

One of the initial outputs of their weekly BSR meetings.

Architects Academy at an insulation manufacturing facility

Programme of technical engagement for aspiring designers.

Building Safety Levy technical consultation response

Details of the planned levy now due in 2026.

Great British Energy install solar on school and NHS sites

200 schools and 200 NHS sites to get solar systems, as first project of the newly formed government initiative.

600 million for 60,000 more skilled construction workers

Announced by Treasury ahead of the Spring Statement.

The restoration of the novelist’s birthplace in Eastwood.

Life Critical Fire Safety External Wall System LCFS EWS

Breaking down what is meant by this now often used term.

PAC report on the Remediation of Dangerous Cladding

Recommendations on workforce, transparency, support, insurance, funding, fraud and mismanagement.

New towns, expanded settlements and housing delivery

Modular inquiry asks if new towns and expanded settlements are an effective means of delivering housing.

Building Engineering Business Survey Q1 2025

Survey shows growth remains flat as skill shortages and volatile pricing persist.

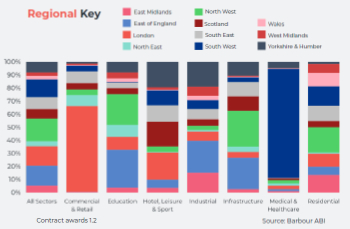

Construction contract awards remain buoyant

Infrastructure up but residential struggles.

Warm Homes Plan and existing energy bill support policies

Breaking down what existing policies are and what they do.

A dynamic brand built for impact stitched into BSRIA’s building fabric.